Kyle Harpin, CFA, CFP

Senior Analyst, Advice & Planning Research

Developing an effective retirement income strategy is more complex than most people anticipate, and even small missteps can meaningfully impact how long your money lasts. You’ve saved diligently for retirement, so it’s natural to want your strategy to be top-notch. Yet many people fall victim to decisions that can reduce their income over time.

Here are four common mistakes investors make when developing a retirement income strategy and actions you can take to help avoid them.

Mistake 1: starting with too high of a withdrawal rate

Withdrawal rates play a critical role in retirement planning. While no single withdrawal rate will work for everyone, it’s important to approach yours with intention. That’s because the amount you withdraw from your portfolio each year is one of the most important factors in determining whether your money lasts as long as you need it.

For example, a new retiree starting with a 3% initial withdrawal rate has about a 90% chance their portfolio will last for 33 years. But at a 5% withdrawal rate, that time frame falls by more than a decade, to 18 years.

Your withdrawal rate is important

Source: Edward Jones estimates. Results using a Monte Carlo simulation of a 50% fixed income/50% stocks portfolio, rebalanced annually. The portfolio includes cash (1%), U.S. investment-grade bonds (39%), U.S. high-yield bonds (10%), U.S. large-cap stocks (33%) and international large-cap stocks (17%). Expected returns based on long-term capital market expectations for cash of 2.9%, U.S. bonds of 3.8% to 5.8%, U.S. large-cap stocks of 7.2% and international large-cap stocks of 7.2%. We also assume an annual fee of 1%. This hypothetical example is for illustrative purposes only and does not reflect the performance of a specific investment.

Here’s what you can do to help improve your strategy

- Start with more conservative withdrawals. While a 4% withdrawal rate may make sense for someone in their mid to late 60s, we don’t recommend it for everyone. It’s important to work with your financial advisor to determine a sustainable withdrawal rate based on your goals and unique circumstances.

- Consider delaying retirement. If you haven’t yet retired and your target withdrawal rate is limiting your portfolio’s longevity, it might be worth considering delaying retirement. Putting off retirement for just a couple years can help you build additional savings, take advantage of catch-up contributions and earn returns to help your portfolio endure.

Calculate your potential retirement savings

Fill in the fields below to get a snapshot of your retirement savings potential.

*Required

Current Age*

(between 1 and 99 years)

Expected Retirement Age*

(between 2 and 99 years)

Beginning Contribution Age*

(between 2 and 99 years)

Investment Rate of Return* i

(between 0.01% and 12%)

Minimum Annual Contribution* i

(between $1 and $9,999,999)

Maximum Annual Contribution*

(between $1 and $9,999,999)

Current Retirement Savings* i

(between $1 and $9,999,999)

Please complete all required fields with valid values.

Your potential yield if you retire at 60

Start contributing at 20 may yield

$0 to $0

Start contributing at 10 may yield

$0 to $0

Will this be enough?

How much you’ll need is driven by how much you plan to spend in retirement. An Edward Jones financial advisor can help you:

- Get a handle on what you spend each year right now.

- Walk through how your expenses may change later in life.

- Identify and factor in outside sources of income such as Social Security.

- See where you stand with your current retirement planning using our established 5-step Process.

Let’s talk. Meet with an Edward Jones financial advisor for a complimentary retirement analysis.

Mistake 2: not being flexible with your strategy

When it comes to the markets, volatility can come out of nowhere and change your circumstances. When the unexpected occurs, flexibility with your strategy can make a difference.

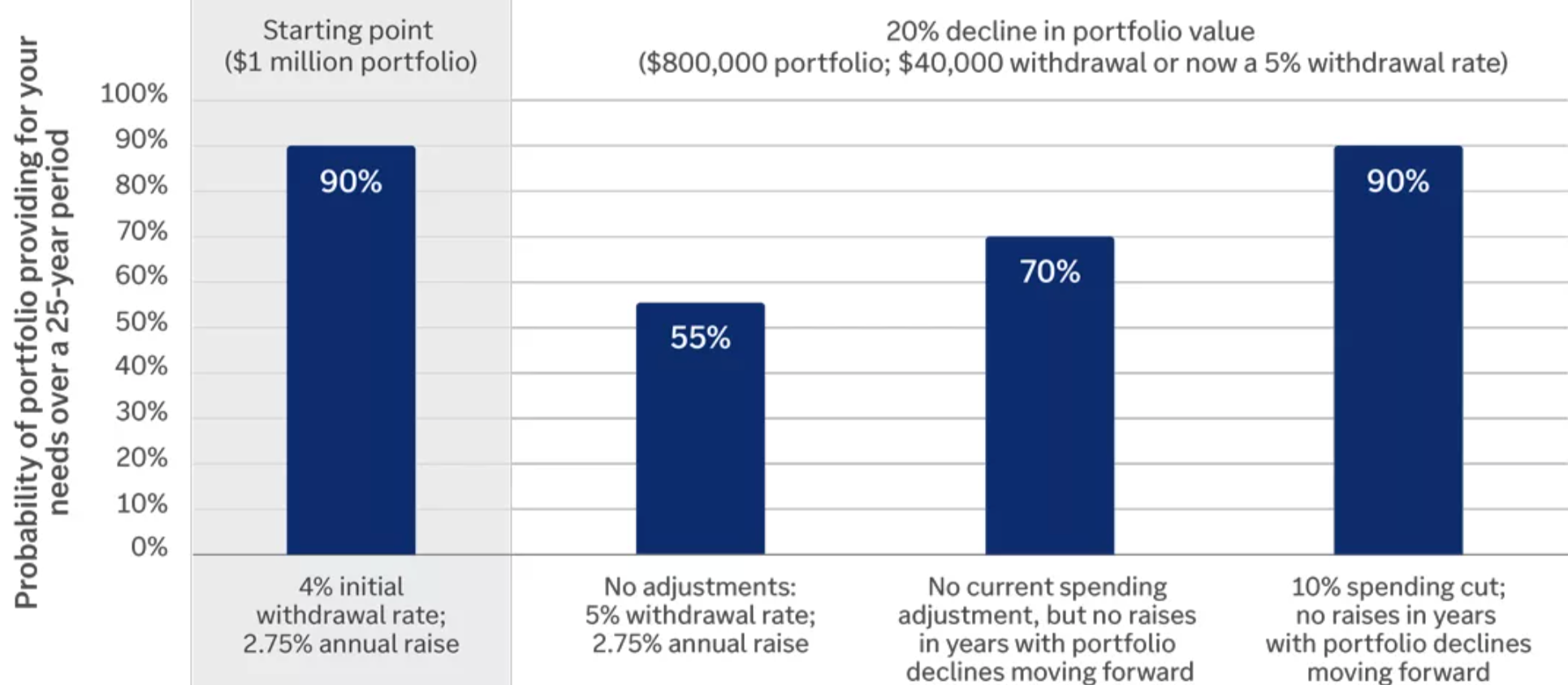

Here’s how this looks in practice: Let’s say you start retirement with a $1 million portfolio and a withdrawal rate of 4% for a total income of $40,000, which increases each year to account for inflation. Now imagine markets decline by 20% and your portfolio is now $800,000. If your spending remains the same, your withdrawal rate has gone from 4% to 5%, and the probability your portfolio lasts for a 25-year retirement falls from almost 90% to less than 55%.

Here’s what you can do to help improve your strategy

- Adjust your spending when markets fluctuate. If you find yourself in the above situation, making two spending changes may help you get back on track. Most strategies incorporate spending increases to account for inflation. But what if you didn’t take an inflation increase in years after your portfolio declined? That alone could help improve your likelihood of success from about 55% to 70%. And coupling it with a one-time 10% cut to your withdrawal could help increase it further to 90%.

- Incorporate flexibility before you need it. Setting aside 12 months of portfolio withdrawals in a separate account for spending, and another three to five years in a short-term fixed-income ladder, can help your portfolio weather market downturns. These funds can provide you with a source to spend from while markets recover. Assuming they do recover, you could refill your spending account and cover some of your current expenses with your portfolio’s growth.

Your behavior can drive your success

Mistake 3: claiming Social Security too early

Another area where timing plays a crucial role is Social Security. The age at which you claim Social Security is important because it affects the size of your benefit paycheck, and the earlier you claim, the lower your monthly benefit will be. A lower benefit also affects other benefits Social Security provides.

Social Security recipients typically receive an annual cost-of-living adjustment (COLA) to account for inflation. However, if you claim benefits earlier, the COLA is applied to a smaller base, so your total paycheck increases by a smaller amount. Conversely, if you delay, you don’t have to worry about missing the COLA because the Social Security Administration still applies an inflation adjustment to your benefit base.

Because claiming early reduces your benefit, it also reduces the survivor benefits that your spouse would receive in the event of your passing. This could impact their ability to make ends meet later in life, potentially adding stress to an already difficult time.

Here’s what you can do to help improve your strategy

- Be intentional about claiming Social Security. While claiming decisions can vary based on your personal circumstances, we typically recommend delaying until your maximum benefit. If you’re claiming Social Security based on your own record, your maximum benefit is achieved at age 70; if you’re claiming on a spouse’s work record, you achieve your maximum benefit at full retirement age (FRA). And if you claim early on a spouse’s record, not only will your benefit be reduced, but any spousal benefit you receive from a higher-earning spouse will be too.

- Incorporate these key factors in your claiming decision. Work with your financial advisor to incorporate your income needs, spouse, life expectancy and employment/income into your claiming decision.

Mistake 4: relying too much on portfolio income

Mistake 4: relying too much on portfolio income

Mistake 4: relying too much on portfolio income

Mistake 4: relying too much on portfolio incomeIn prior generations, retirement income was typically made up of three sources: Social Security, a pension and portfolio income.

While Social Security and portfolio income are still broadly present, the prominence of pensions has declined, putting more pressure on portfolios to generate retirement income. As a result, understanding how much of your income depends on your portfolio has become increasingly important.

The amount you rely on your savings for income can be measured by your reliance rate. It’s calculated by dividing the amount of income that comes from your portfolio by your total retirement income. A higher reliance rate can be problematic because it can cause your strategy to be more sensitive to market fluctuations.

Here’s what you can do to help improve your strategy

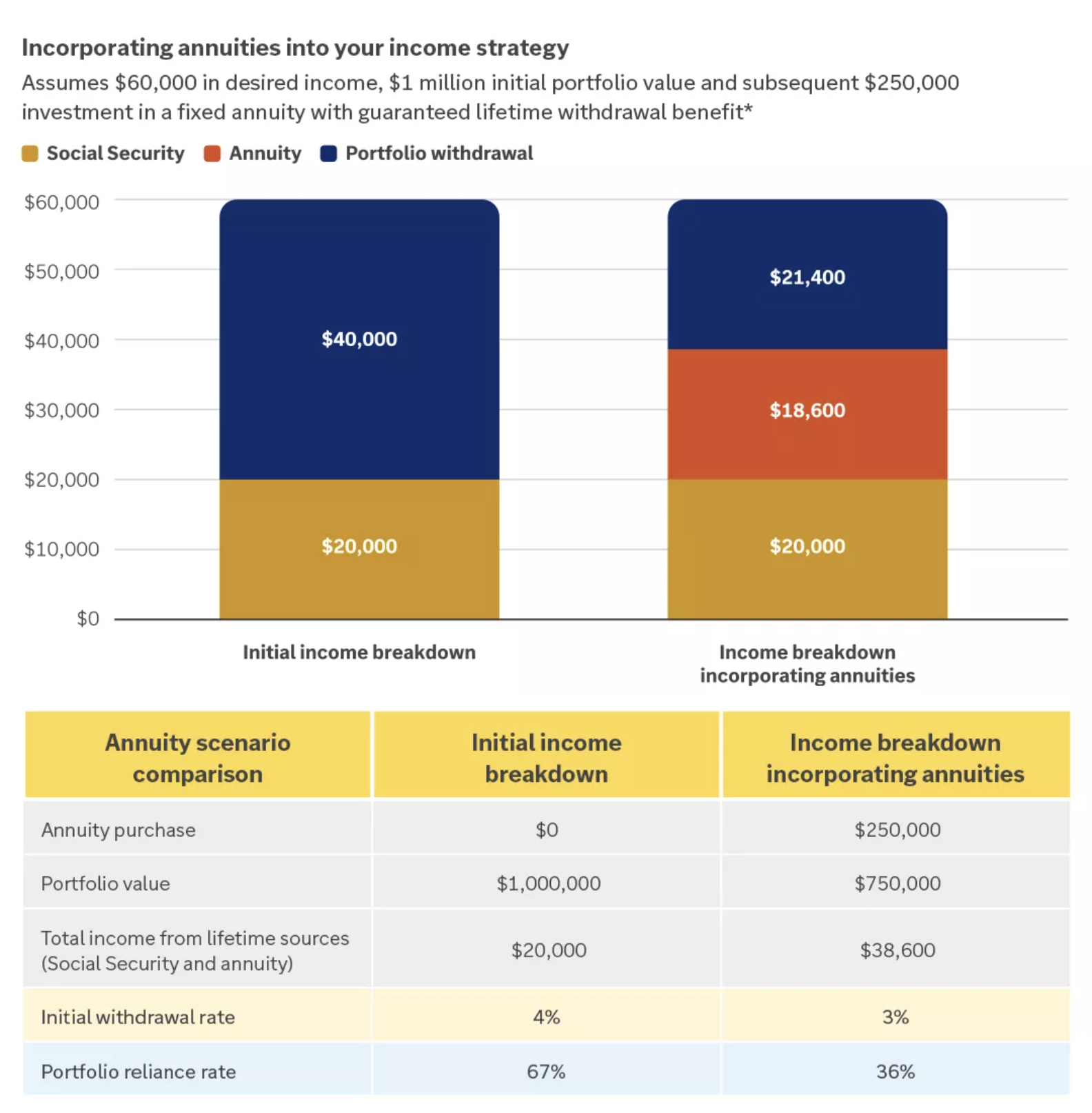

- Consider a protected lifetime annuity.* With an annuity, you exchange a portion of your portfolio for a guaranteed stream of income from an insurance company, which helps replicate the cash flow from a missing pension. The example below highlights how an annuity can help reduce both your reliance rate and initial withdrawal rate, in turn helping your strategy be less sensitive to the markets and increase your portfolio’s longevity.

- Adhere to time-tested investing principles. Investing in a diversified set of quality investments with a long-term focus won’t necessarily cause you to rely less on your portfolio, but it should help you feel more confident in your portfolio. This can help you view it as a more reliable source of income than it would be otherwise.

Source: Edward Jones.

Source: Edward Jones.

*Fixed annuity with guaranteed lifetime withdrawal benefit from RightBridge on 10/1/2025. Assumes male annuitant purchasing and taking income from a $250,000 annuity at age 65, Missouri resident. Assumes $20,000 Social Security income, rounded to nearest $100. Example is for illustrative purposes only and does not reflect a specific investment. Guarantees are subject to the claims-paying ability of the issuing life insurance company.

How Edward Jones can help

Retirement is one of life’s biggest transitions, and the decisions you make today can influence your financial strategy for years to come.Your unique circumstances will help inform the appropriate strategy for you, which is why we recommend working with your financial advisor to build a retirement income plan that reflects what matters most to you.

Important information:

*Annuities are long-term investments designed to provide income during retirement. Guarantees are subject to the claims-paying ability of the issuing life insurance company.

Edward Jones is a licensed insurance producer in all states and Washington, D.C., through Edward D. Jones & Co., L.P, and in California, New Mexico and Massachusetts through Edward Jones Insurance Agency of California, L.L.C.; Edward Jones Insurance Agency of New Mexico, L.L.C.; and Edward Jones Insurance Agency of Massachusetts, L.L.C.

Content is intended as educational only and should not be interpreted as a specific recommendation or investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.